Deep Price Cuts Lead the Charge

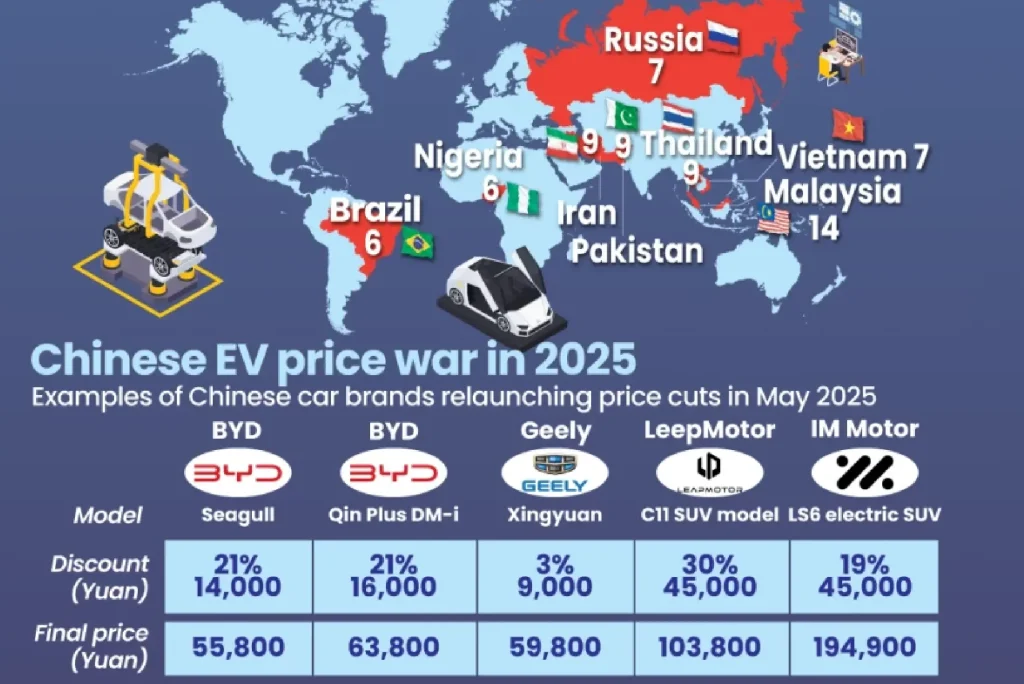

China’s electric vehicle (EV) sector has entered a fierce pricing battle, with major manufacturers slashing prices in a bid to attract cost-conscious consumers and maintain their market positions. Leading the charge is BYD, China’s top EV manufacturer, which recently cut prices on over 100 of its models.

Notably, the compact Seagull hatchback is now priced under $10,000, making it one of the most affordable EVs globally. Meanwhile, the popular Qin Plus sedan received a 20% price reduction, now selling for just 79,800 yuan (about $11,000). These aggressive price strategies aim to broaden EV adoption across China’s vast second-tier cities and rural markets, where consumers remain price-sensitive and traditionally loyal to internal combustion engine (ICE) vehicles.

Wider Industry Follows Suit

Following BYD’s lead, a wave of domestic automakers including SAIC-GM-Wuling, Changan Automobile, and Hozon New Energy have entered the price war. These companies are now offering small to mid-size EVs below the symbolic 100,000 yuan ($13,800) threshold.

Many of these vehicles target first-time car buyers or families looking for economical second vehicles. While this price point was once thought to be financially unsustainable, these brands are leveraging scale, in-house battery development, and simplified production processes to keep costs low while maintaining competitiveness.

Falling Battery Costs and End of Subsidies Drive Pricing Strategy

Several structural shifts are enabling this drop in EV prices. Most significantly, the cost of lithium-ion batteries, which make up a substantial portion of an EV’s cost, has declined sharply due to technological advancements and improved supply chain efficiencies.

At the same time, Chinese government subsidies, which previously helped offset the price of EVs, officially ended in late 2022. Without state support, automakers are being forced to offer direct discounts or risk losing customers to competitors.

Additionally, with over 200 EV brands in China, the market is approaching saturation, especially in major cities. Automakers are now shifting focus to lower-tier cities and smaller markets, where EV penetration is still growing but highly dependent on price sensitivity.

Profit Margins Hit Historic Lows

While great for consumers, the price war is proving painful for automakers’ bottom lines. Industry-wide profit margins have plummeted to 5%, their lowest level in over a decade. This squeeze on profitability is unsustainable for smaller players who lack the scale or financial strength to absorb losses.

Analysts predict a looming wave of consolidation, where weaker brands will either be absorbed by larger companies or forced to exit the market entirely. Larger, well-capitalized firms like BYD, Nio, and Geely are expected to weather the storm, while startups and niche brands may struggle to survive.

A Global Impact: Chinese EVs Go Abroad

This price competition is no longer limited to China’s domestic market. With EV adoption accelerating worldwide, Chinese automakers are looking outward for growth. Brands like BYD, MG (under SAIC), and Great Wall Motors are now expanding aggressively into Southeast Asia, Latin America, and Europe, often undercutting Western rivals on price while offering competitive technology and features. This is putting immense pressure on traditional automakers like Toyota, Volkswagen, and Ford, which are still transitioning their lineups from combustion to electric.

The ability of Chinese companies to produce high-quality EVs at lower prices is quickly becoming a global advantage—one that is redefining competitive dynamics in the automotive industry.

Conclusion: An Industry at a Crossroads

China’s EV price war is more than just a temporary sales tactic—it signals a long-term transformation of the industry. Automakers are being pushed to become more efficient, innovative, and aggressive in capturing market share, both at home and abroad. While consumers benefit from more affordable electric vehicles, the broader market may see significant shifts in brand dominance, supply chain control, and even global pricing norms.

As the dust settles, only the most adaptable and strategically prepared companies are likely to thrive. The outcome of this price war could determine who leads the global EV market in the decade to come.